🔍 Affordability Isn’t a Feeling—It’s a Formula

San Diego’s housing market has changed in price, but not in burden. For decades, affordability has been framed as a moving target, but the math shows a consistent pattern: the percentage of income required to own a home has remained nearly the same.

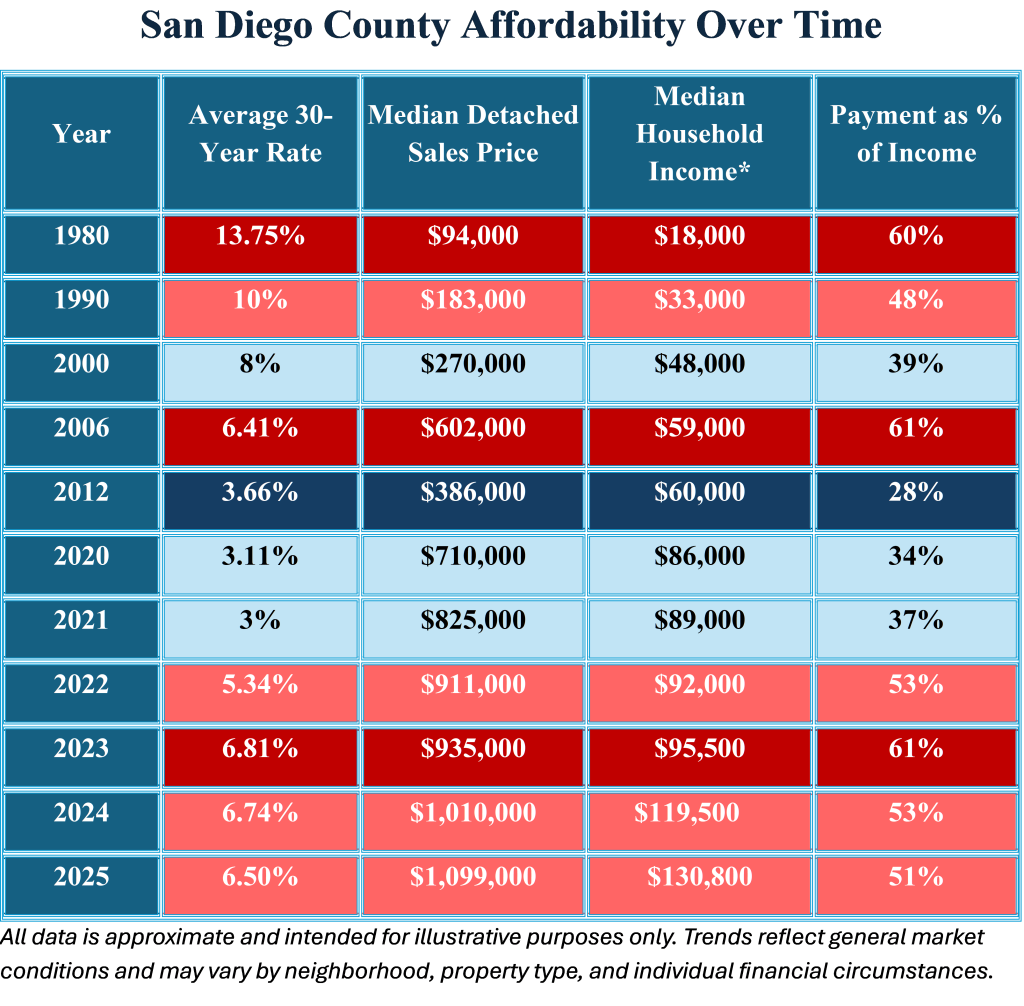

🧮 Same Burden, Different Decade

We hear it all the time:

“I wish I could’ve bought a house back in the ’80s when prices were low.”

Let’s look at that.

1980

- Median home price: $94,000

- Interest rate: 13.75%

- Median income: $18,000

- Monthly mortgage payment ≈ $1,078

- Annual cost ≈ $12,936

- Payment as % of income: 60%

2025

- Median home price: $1,099,000

- Interest rate: 6.50%

- Median income: $130,800

- Monthly payment ≈ $5,561

- Annual cost ≈ $66,732

- Payment as % of income: 51.0%

The numbers show it clearly: the financial burden of homeownership hasn’t disappeared—it’s shifted. Lower prices in the past came with lower incomes and higher rates. Today’s higher prices are paired with higher incomes and lower rates. The result? Nearly the same percentage of income required to buy.

🧠 Nostalgia vs. Reality

Wishing for 1980 prices means giving up 2025 income. That’s the trade-off. You can’t cherry-pick one side of the equation. If you want a $94,000 home, you also have to accept an $18,000 salary and a 13.75% interest rate.

What’s changed isn’t the burden—it’s the tools.

- In the ’80s, buyers had to save 20% down—that’s nearly $19,000 on a $94,000 home.

- Today, buyers can get in with 3% down and use down payment assistance programs that didn’t exist back then.

- A 3% down payment on a $600,000 home is $18,000—the same cash requirement as 1980, but with far more income to support it.

💡 Renting Is Still Paying a Mortgage—Just Not Yours

Let’s be blunt: renters are already paying mortgage-sized amounts every month. The only difference is that the equity goes to someone else.

- If your rent is $3,000/month, that’s $36,000/year.

- That’s enough to cover the mortgage on a $600,000–$700,000 home with today’s rates and programs.

- The question isn’t can you afford to buy—it’s are you ready to stop paying someone else’s mortgage?

🔥 What This Means for San Diego Families

🛠️ How Homeownership Is Still Possible Today

- Lower Down Payments: Unlike previous generations who had to save 20% just to qualify, today’s buyers can access 3% down conventional loans, FHA programs, and state/local down payment assistance. That means a buyer could enter the market with as little as $18,000 on a $600,000 home—the same cash requirement as in 1980, but with far more income to support it.

- Flexible Financing Options: Programs now exist for first-time buyers, veterans, teachers, and low-to-moderate income households. These aren’t gimmicks—they’re strategic tools designed to reduce barriers to entry.

- Rent Equivalency: Many renters are already paying $3,000–$4,000/month. That’s equivalent to the mortgage on a $600,000–$800,000 home. The difference? Rent builds nothing. Mortgage builds equity, stability, and long-term financial leverage.

📊 What the Data Actually Shows

- The Burden Is Consistent: Whether it’s 1980 or 2025, the percentage of income required to own a home has hovered around 50–60%. That means today’s buyers aren’t facing a new crisis—they’re facing the same proportional challenge their parents did.

- Income Growth Offsets Price Growth: While home prices have increased, so have incomes. In 1980, a $94,000 home required 60% of an $18,000 income. In 2025, a $1.1M home requires 51% of a $130,800 income. The math holds.

- Ownership Is Still a Strategic Move: Even with higher prices, buyers today have more tools, more flexibility, and more income. Ownership remains one of the most powerful ways to protect against inflation, rent hikes, and displacement.

💬 Why Waiting Can Cost More Than Buying

- Missed Appreciation: San Diego homes have appreciated dramatically over time. Waiting for prices to drop often means missing out on equity gains that could’ve been yours.

- Rising Rents: Rent rarely goes down. While buyers can lock in a fixed mortgage, renters are exposed to annual increases with no return on investment.

- Lost Leverage: Homeownership builds credit, stability, and generational wealth. Every year spent renting is a year of lost leverage—financial, legal, and emotional.

- Market Manipulation: Headlines often push fear or false hope. “Affordability is improving” or “Prices will crash soon” are narratives designed to drive clicks, not guide families. The truth is in the ratios—and those ratios say: the burden is consistent, and the opportunity is real.

🧭 Final Thought: Ownership Isn’t About Timing—It’s About Strategy

The numbers don’t lie. Whether it’s 1980 or 2025, the percentage of income needed to own a home has stayed consistent. What’s changed is the access, the tools, and the opportunity to build equity faster and smarter.

If you’re renting, you’re already paying a mortgage—just not yours. If you’re waiting for prices to drop, you may be trading short-term hesitation for long-term loss. And if you’re comparing today’s market to your parents’ era, make sure you’re comparing the full picture—not just the price tag.

We’re not here to convince you. We’re here to equip you—with facts, clarity, and strategy. Whether you’re buying your first home, navigating Prop 19, or protecting family equity through probate, we’ll help you move forward with confidence.

Because ownership isn’t about nostalgia—it’s about knowing your numbers and owning your future.

🛡️ What We Fight For

We don’t sell homes—we clarify systems. We don’t push deals—we protect equity. Every data point above reflects a consistent truth: the cost of ownership, relative to income, has remained stable across generations. If you’re navigating a complex transition—probate, pre-foreclosure, Prop 19—we’re here to help you make decisions based on facts, not nostalgia.

Why Work With Us?

We do our best:

✔️ To ensure your sale or purchase is legal, safe, and protected

✔️ To prevent the expensive mistakes others miss

✔️ We fight to maximize your profit and protect your future

✔️ We’re not here for fluff—we’re here to deliver results with integrity

💼 HomesinSDCounty: Local Power. Nationwide Reach.

✅ Experts in Probate, Rightsizing, Pre-Foreclosure & Distressed Sales

✅ Strategic Advisors in Residential, Investment & Commercial Real Estate

✅ No fluff. Just relentless advocacy and smart protection.

💥 Explore Our Valuable FREE Real Estate Resources

✓ eBooks | ✓ Checklists | ✓ Buying & Selling Guides | ✓ Investor Tools

→ Visit our Resources Page to download now

🛫 Relocating? Buying, selling, or relocating in San Diego, Riverside, Orange County—or anywhere in the U.S.?

We’ve Got You Covered—Nationwide.

We’re not just your local experts—and we don’t just work in Southern California. We’re backed by the powerhouse Coldwell Banker National Network and a handpicked team of personally vetted agents across the country. Whether you’re making a move across town or across the country, we ensure a smooth, strategic, and successful experience.

We’ll connect you with an agent we trust—not just someone in the directory.

📲 Brad & Karen Mattonen

HomesinSDCounty | Coldwell Banker West

858-518-2875 | www.homesinsdcounty.com

Your Smart Move—Wherever Life Takes You