Wildfire rules are changing across all of San Diego County — and insurance companies are enforcing them faster than cities can update their codes. Whether you live in San Diego, Vista, Oceanside, Fallbrook, Poway, or Temecula, the new 0–100 foot standards will impact your home, your insurance, and your equity.

California’s wildfire‑prevention rules are shifting fast — and the impact is hitting homeowners across all of San Diego County, not just within the City of San Diego.

Between the City’s new Zone Zero ordinance, the letters circulating in Vista and other North County communities, and the wave of insurance non‑renewals, one thing is clear:

This is no longer a city‑by‑city issue. It’s a countywide, statewide, insurance‑driven mandate — and every homeowner in a Very High Fire Hazard Severity Zone (VHFHSZ) will be affected.

If your home sits in the Very High Fire Hazard Severity Zone (VHFHSZ) Areas — and thousands of homes across San Diego, North County, and the Inland Corridor do — these rules apply to you whether you live in:

San Diego • Vista • Oceanside • Fallbrook • Bonsall • Escondido • San Marcos • Poway • Rancho Bernardo • 4S Ranch • Rancho Peñasquitos • Valley Center • Temecula • Murrieta • Wildomar • Menifee • San Clemente (east)

This guide breaks down what’s happening, why it’s happening, and what homeowners must do to protect their homes, insurance, and equity.

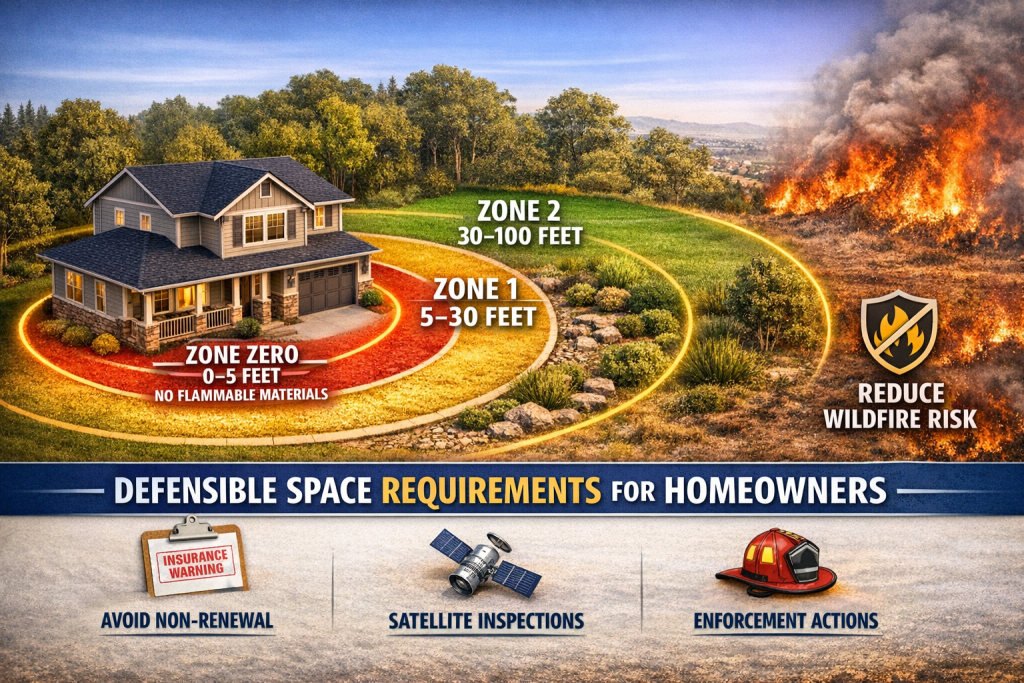

🔥 What Zone Zero Actually Requires (0–5 Feet)

Zone Zero is the first five feet around your home, the area most likely to ignite from wind‑blown embers. Under the new rules, homeowners must remove or replace:

- Wood fencing touching the home

- Mulch and flammable ground cover

- Combustible plants and shrubs

- Wood decks or patios attached to the structure

- Stored items that could ignite

San Diego has formally adopted this requirement. The rest of California will follow by 2025–2026.

🌲 But the Rules Don’t Stop at 5 Feet — They Extend to 100 Feet

Zone Zero is in addition to, not instead of, California’s existing defensible‑space laws:

- Zone Zero (0–5 feet): No flammable materials

- Zone 1 (5–35 feet): Reduced vegetation, spacing, ladder‑fuel removal

- Zone 2 (35–100 feet): Thinning, clearance, ongoing maintenance

This is why letters, notices, and insurance inspections reference more than just the first five feet.

🏡 Vista’s Letter Is Not Unique — It’s the First of Many

Vista’s Letter Isn’t an Outlier — It’s the First Wave

The letter circulating in Vista is not a San Diego ordinance — but it uses the same language because the underlying rules are statewide. Vista is simply the first community where homeowners are seeing the notices, not the only one.

More cities will follow as:

- Statewide Zone Zero standards roll out

- Fire departments update defensible‑space enforcement

- Insurance companies tighten underwriting

- HOAs begin adopting their own compliance rules

- Vista is under statewide defensible‑space laws

- Zone Zero is being implemented statewide

- Insurance companies are enforcing all three zones

- Cities are warning homeowners early to avoid insurance loss

Vista is simply the first community where homeowners are seeing the letters — not the last.

Expect similar letters in:

Escondido • San Marcos • Poway • Rancho Bernardo • Oceanside • Fallbrook • Temecula • Murrieta • Valley Center

…and more.

🧨 The Real Enforcer: Insurance Companies

Insurance Companies Are the Real Enforcers — Not the Cities

Insurance companies don’t care what city you live in. They care about fire‑hazard severity zones, not municipal boundaries.

Carriers are already enforcing:

- Zone Zero (0–5 feet)

- Zone 1 (5–35 feet)

- Zone 2 (35–100 feet)

They use:

- Satellite imagery

- LIDAR

- Vegetation‑density scoring

- Ember‑exposure modeling

- 0–100 foot defensible‑space analysis

This is why homeowners across the county are receiving:

- Non‑renewals

- Mitigation demands

- Inspection photos

- “Fix this or lose coverage” notices

Even when their city hasn’t passed a Zone Zero ordinance.

💸 What Compliance Will Cost

San Diego estimates $2,000–$20,000 per home, depending on:

- Lot size

- Fencing materials

- Landscaping

- Proximity of mature trees

- Required retrofits

Most homeowners will fall on the lower end if they start early.

🧭 What Homeowners Should Do Now (0–100 Foot Checklist)

1. Start with the first 5 feet

Remove flammable materials touching the home.

2. Evaluate fencing

Replace wood fencing that connects directly to the structure.

3. Replace mulch near the home

Use gravel or non‑combustible alternatives.

4. Review Zones 1 & 2

Thin, space, and remove ladder fuels.

5. Document everything

Insurance carriers increasingly require proof.

6. Plan upgrades over time

Spread costs over 2024–2027.

🧩 How We Help Homeowners Navigate This

At HomesInSDCounty, we guide homeowners through:

- Fire‑risk and defensible‑space assessments

- Insurance‑readiness checklists

- RESPA‑compliant vendor referrals

- Equity‑protection strategies

- Pre‑sale Zone Zero compliance planning

- Understanding how Zone Zero interacts with Prop 19, Prop 13, and relocation decisions

This is not just a fire‑safety issue — it’s a real estate, insurance, and financial‑planning issue.

❓ Frequently Asked Questions About Zone Zero & Insurance Enforcement

What is Zone Zero in wildfire safety?

Zone Zero is the first 0–5 feet around your home. This area must be completely free of flammable materials — including wood fencing touching the house, mulch, and combustible plants — to reduce ember ignition risk.

Does Zone Zero apply outside the City of San Diego?

Yes. Zone Zero is part of California’s statewide defensible‑space standards and applies to all homes in Very High Fire Hazard Severity Zones, including Vista, Oceanside, Fallbrook, Poway, Escondido, Temecula, and more.

How are insurance companies enforcing wildfire rules?

Carriers use satellite imagery, vegetation scoring, and ember‑exposure modeling to evaluate compliance with 0–100 foot defensible‑space rules. Non‑compliance can trigger non‑renewals or required mitigation.

What should sellers do before listing?

Sellers should ensure Zone Zero and defensible‑space compliance to avoid insurance issues, protect equity, and attract qualified buyers. Pre‑listing mitigation can improve marketability and reduce surprises during escrow.

Can buyers be denied insurance due to wildfire risk?

Yes. Buyers may face limited insurance options or higher premiums if the property does not meet defensible‑space standards. Some may be forced into the California FAIR Plan, which is more expensive and offers limited coverage.

📞 If you need help navigating these changes — whether you’re preparing your home, planning to sell, or dealing with insurance challenges — we’re here to guide you.

💥 Explore Our Valuable FREE Real Estate Resources

✓ eBooks | ✓ Checklists | ✓ Buying & Selling Guides | ✓ Investor Tools

→ Visit our Resources Page to download now

Brad Mattonen, REALTOR® | CA DRE #02062665 Karen Mattonen, REALTOR® | CA DRE #02044711 Coldwell Banker West | HomesInSDCounty Serving San Diego, Riverside & Orange Counties

Why Work With Us: Trusted advocates. Statute‑level expertise. Equity‑focused strategy. Your next chapter deserves clarity, protection, and a plan.

Your next chapter deserves clarity, protection, and a plan.

🔗 Follow Us Everywhere!

Get daily market updates, home tours, and no-nonsense real estate advice:

- 📺 YouTube: Subscribe for Weekly Updates

- 👤 Facebook: North County SD Home Sales

- 📸 Instagram: @sandiegocountyhomes

- 📌 Pinterest: San Diego Living & Real Estate

- 🎵 TikTok: @homesinsandiegocounty

- 🐦 X (Twitter): @SDHomesForSale

- 💼 LinkedIn: Brad Mattonen – Professional Insights